Published Mon, May 4 2026 by Jessica Dickler

- When it comes to starting salaries, graduates in the Class of 2026 may have to lower their expectations.

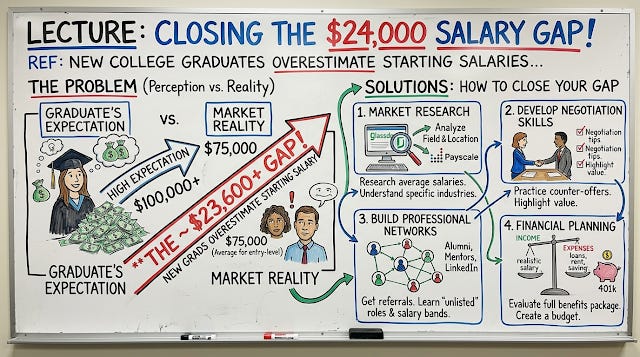

- College students expect to make $80,000 on average one year after graduation, one recent report found. The average salary for new grads is about 30% lower.

- Although pay expectations may be high, the average starting salary for this year’s crop of graduates is rising, other data shows.

It’s a challenging labor market for those just starting out, and new job seekers will likely have to recalibrate their earning potential.

Today’s college seniors expect to make about $80,000 one year after graduation, according to a survey of undergraduates pursuing a bachelor’s degree by real estate site Clever in February and March.

Yet, the average starting salary for recent graduates is $56,153, Clever found, a difference of nearly $24,000.

More than 3 million new graduates enter the workforce every year, banking on the idea that a college degree is the ticket to a well-paying job.

However, this year, those armed with a newly minted diploma have faced one of the toughest job markets in years.

A shaky outlook for jobs

As the artificial intelligence boom reshapes the workforce, some large employers have said they’re replacing entry-level positions with AI in order to streamline operations and cut costs. Concerns about the economy and persistent inflation are also causing some companies to put hiring plans on hold.

Amid a shaky job market, rising tuition and ballooning student loan balances, more young adults are questioning whether a college degree is worth it, several studies show. At the same time, students across majors overestimated the future value of their degrees, Clever found.

Engineers, for example, expected a starting salary of $92,452, according to Clever, nearly 20% more than they are likely to earn one year after graduating.

The path to financial security

For many young adults, future earnings are key to achieving independence. Largely because of economic pressures, more recent grads have had to lean on their families for financial support years after getting their degree.

These days, about half of parents — a record high — are pitching in to help, including paying essential monthly expenses, such as groceries, utilities and rent, according to one 2025 report by Savings.com.

The disconnect between perception and reality only worsens over time. Students anticipate that a decade into their careers they will make $144,889 on average. That’s well over the average midcareer salary of $95,521, according to Clever.

On the upside, the unemployment rate among college graduates with a bachelor’s degree is under 4%, according to March data from the U.S. Bureau of Labor Statistics. Employers plan to hire about 5.6% more new grads from this year’s class than they hired from the class of 2025, according to a report from the National Association of Colleges and Employers.

“Those employers who are increasing cite company growth and the commitment to succession planning as their main reasons for increasing their new college graduate hires,” said Andrea Koncz, NACE’s senior research manager.

Rising starting salaries

Although pay expectations may be off base, compared with last year, the average starting salary for this year’s crop of graduates is mostly higher across majors, according to a separate survey by NACE.

“The outlook appears to be slightly better for this year’s class in terms of both hiring and salaries,” Koncz said.

The overall average salary for new grads rose 5.5% to $68,873 from $65,276, NACE found, while typically high-paying disciplines, such as engineering or computer science, continued to notch gains.

Computer science graduates are projected to be the highest paid of all majors for the Class of 2026, with average salaries up 6.9% to $81,535 from $76,251 in 2025. The overall average salary for engineering graduates, the second-highest-paid, currently stands at $81,198.

Starting salaries for new grads, or adults between the ages of 20-24, at small and medium-sized businesses have bumped up as well, averaging $65,734 for the Class of 2026, up from 62,801 a year ago, according to data from payroll provider Gusto.

Kyle Fox, the director of Alopex ID, a digital marketing agency based in Palmer, Alaska, says starting salaries for entry-level positions at his firm are around $45,000 a year, although they can rise to nearly $70,000 after a few years.

New hires are “generally happy to have a job,” Fox said. “If you come out with a degree in media, especially up here in Alaska, entry-level positions are few and far between.”

In fact, 67% of new college grads said they would trade higher pay for job security, according to Monster’s recent State of the Graduate report. The jobs platform surveyed more than 1,000 recent and soon-to-be graduates.

***** ***** ***** ***** *****

Source: CNBC

https://www.cnbc.com/2026/05/04/college-grads-overestimate-starting-salaries.html